Related Expertise: Business Transformation , Post-Merger Integration , Corporate Finance and Strategy

Lessons from Eight Successful M&A Turnarounds

November 12, 2018 By Ib Löfgrén , Lars Fæste , Tuukka Seppä , Jonas Cunningham , Niamh Dawson , Daniel Friedman , and Rüdiger Wolf

M&A is tough, especially when it involves an underperforming asset that needs a turnaround. About 40% of all deals, on average, require some kind of turnaround, whether because of minor problems or a full-blown crisis. With M&A valuations now at record levels, companies must pay higher prices simply to get a deal done. In this environment, leaders need a highly structured approach to put the odds in their favor.

The greatest M&A turnarounds

Automotive: groupe psa + opel, biopharmaceuticals: sanofi + genzyme, media: charter communications + time warner cable + bright house networks, industrial equipment: konecranes + mhps, retail grocery: coop norge + ica norway, shipbuilding: meyer werft + turku shipyard, retail: office depot + officemax, energy: vistra + dynegy.

We recently analyzed large turnaround deals—those in which the target was at least half the size of the buyer in terms of revenue, with the target’s profitability lagging its industry median by at least 30%. Our key finding was that these deals can be just as successful as smaller deals that don’t require a turnaround in terms of value creation. However, they have a much greater variation in outcomes. In other words, the risks are greater and the potential returns are also greater. Critically, our analysis identified four key factors that lead to success in turnaround deals.

1. These buyers use a “full potential” approach to identify all possible areas of improvement. Rather than merely integrating the target company to capture the most obvious synergies, a full-potential approach generates improvements to the target company, captures all synergies, and capitalizes on the opportunity to make needed upgrades to the acquirer as well. (See the exhibit.)

Copy Shareable Link

2. These buyers have a clear rationale for how the deal will create value, and they take a structured, holistic approach:

- They initially fund the journey by generating quick wins that deliver cash to the bottom line quickly, typically restructuring back-end operations to reduce costs and increase efficiency.

- Then they pivot from cost-cutting to growth measures in order to win in the medium term. They revamp the portfolio, selling off some business units and assets and buying others that align with their strategic direction.

- Finally, they invest in the future, often focusing on building digital businesses, upgrading processes with AI, and investing in R&D to secure long-term growth and expanding margins.

Winning buyers have a clear rationale, execute with rigor and speed, and address culture upfront.

3. Successful acquirers execute their plan with rigor and speed. They begin developing plans long before the deal closes, so that they can begin implementation on day one, seamlessly combining the core elements of post-merger integration and a turnaround program. These acquirers are extremely diligent in building clear milestones and objectives into the plan to ensure that key integration and improvement steps are achieved on time. Throughout the process, they move as quickly as possible, regarding speed as their friend. Moreover, they are confident enough to make their targets public and to systematically report on progress.

4. Winning acquirers address culture upfront by reorienting the organization around collaboration, accountability, and bottom-line value. Culture can often be hard to quantify or pin down, but it’s critical in shaping a company’s performance following an acquisition. (See Breaking the Culture Barrier in Postmerger Integrations , BCG Focus, January 2016.)

The case studies on the following pages illustrate these four principles. They offer clear evidence that M&A-based turnarounds may be hard but carry significant opportunity when done right.

Groupe PSA, the parent company of Peugeot, Citroën, Vauxhall Motors, and DS Automobiles, was languishing after the 2008 financial crisis. Demand was particularly slow to recover in Europe, which accounted for more than two-thirds of the company’s sales. After losing $5.4 billion in 2012 and $2.5 billion in 2013, Groupe PSA struck a deal to sell 14% of the company to Chinese competitor Dongfeng and another 14% to the French government, for $870 million each. With the capital raised, it launched a turnaround program in 2014. As part of the program, Groupe PSA bought the Opel brand, which had lost about $19 billion since 1999, from General Motors. The deal was finalized in August 2017.

The turnaround has a strong growth element with a focus on strengthening brands. A sales offensive was built on reducing the variety of models available, offering more attractive leases (possible thanks to the company’s stronger financial services capability), and maintaining discount discipline. Cost efficiency is another important element. Limiting the number of models reduces complexity across the combined group, which reduces costs in both manufacturing and R&D. The increased scale across fewer models leads to simpler procurement and more negotiating clout with suppliers.

The turnaround continued at a relentless pace through the first half of 2018, with profitability restored at Opel and margins continuing to rise for Groupe PSA as a whole.

Overall, gross margins have increased by 35% since 2013. During the same period, Groupe PSA has rebounded from losing money to an EBIT margin of 6%, in line with competitors such as General Motors and ahead of Hyundai and Kia. Perhaps most impressive, the company’s market cap has increased more than 700%. In all, the transformation has allowed Groupe PSA to resume its position as one of the top-performing automakers in the world.

Key success factors in this turnaround: Groupe PSA started the turnaround by raising capital to fund the journey. That enabled it to buy GM’s Opel unit, halt steep financial losses quickly, and generate a profit within one year of the acquisition.

Raising capital allowed Groupe PSA to buy GM’s Opel unit and generate a profit within one year.

In 2009, French pharmaceutical company Sanofi was in acquisition mode. Many of its products were losing patent protection, and the company wanted to shift from traditional drugs into biologics. One potential target was Genzyme.

From 2000 through 2010, Genzyme had grown rapidly, but manufacturing issues at two of its facilities halted production and led to a shortage of key drugs in its portfolio. Sales plunged, the US Food and Drug Administration issued fines, and investors called for management changes. But many features of the company still met Sanofi’s needs, including a lucrative orphan drug business with no patent cliff and a strong history of innovation. Sanofi made an offer: $20 billion, or $74 per share, which was roughly Genzyme’s value before the manufacturing problems hit.

Management laid out a bold ambition and moved fast. The company streamlined manufacturing, opening a new plant to reduce the drug shortage and simplifying operations to remove bottlenecks at existing plants. Next, it moved sales and marketing for some of Genzyme’s businesses, including oncology, biosurgery, and renal products, under the Sanofi brand. It also reduced the overall sales force by about 2,000 people.

Genzyme’s R&D pipeline was integrated into Sanofi, and a new portfolio review process led to the cessation of some studies and the reprioritizing of others. And about 30% of Genzyme’s cost base was reduced through the integration with Sanofi. Genzyme’s diagnostics unit was sold off, and about 8,000 full-time employees were eliminated in the EU and North America.

The moves generated positive results fast. Overall, the integration led to about $700 million in cost reductions through synergies. By 2011, the company was back in expansion mode with 5% revenue growth, increasing to 17% in 2012. Only about 13% of Sanofi’s revenue came from Genzyme products, but these were poised for strong growth, positioning Sanofi as a global leader in rare-disease therapeutics and spurring its evolution into a dominant player in biologics.

Key success factors in this turnaround: Sanofi laid out a bold ambition in its acquisition of Genzyme, and it executed a strategic repositioning with extreme speed, cutting costs and increasing top-line growth.

Genzyme executed a strategic repositioning with speed, cutting costs and increasing top-line growth.

With 8% of the US market in 2014, cable TV provider Charter Communications found itself facing fierce competition for multichannel video subscribers, who usually had bundled services with increasingly important broadband subscriptions. The threat came not only from other multichannel video providers in its markets—including direct-broadcast satellite services and large telcos—but from internet streaming services, as many cable subscribers were “cutting the cord” and streaming video over mobile and other devices.

To protect its market share and profits, Charter significantly expanded its subscriber base in 2015 by acquiring Time Warner Cable and Bright House Networks, which had a 20.8% and 3.6% share of the US cable market, respectively, paying $67 billion for the two businesses. The acquisitions made Charter the second-largest broadband provider and the third-largest multichannel video provider in the US.

With the deal closed, Charter launched a bold transformation that captured extensive synergies among the three businesses in areas such as overhead, product development, engineering, and IT, and it introduced uniform operating practices, pricing, and packaging. Most important, the company’s increased scale improved its bargaining power with content providers. Charter went beyond synergies in a full-potential plan to accelerate revenue growth, product development, and innovation through the increased scale, improved sales and marketing capabilities, and enhanced cable TV footprint brought about by the combination of the three companies. It improved products and services, centralized pricing decisions, and streamlined operations to achieve additional operating and capital efficiency.

As a result, Charter kept up its premerger growth trend and profitability, growing at an annual rate of 5.5% post-merger to reach $42 billion in revenues in 2017. In addition, Charter’s value creation significantly outperformed that of its peers, increasing annualized TSR to 289% from the closing of the transaction to the end of 2017.

Key success factors in this turnaround: Charter made a bold move in acquiring both Time Warner Cable and Bright House Networks. Management developed an extensive plan to generate operational synergies and rationalize the commercial offering of the new entity.

Charter developed an extensive plan to generate operational synergies and rationalize the new entity’s offering.

Konecranes is a global provider of industrial and port cranes equipment and services. Several years ago, in the face of increased competition, Konecranes was struggling to cut costs or grow organically. In 2016, it bought a business unit from Terex Corporation called Material Handling & Port Solutions (MHPS), its principal competitor. The MHPS business included several brands that complemented Konecranes’ products and services, along with some sizeable overlaps in technology and manufacturing networks.

Before the deal closed, Konecranes drafted an ambitious full-potential plan to generate about $160 million in synergies within three years through cost reductions and new business. That represented a 70% improvement over the joint company’s pro forma financials. The turnaround plan encompassed all main businesses and functions across both legacy Konecranes and MHPS operations.

As part of the preclose planning, Konecranes’ leaders designed an overall transformation to start after the merger was finalized. The program covered all business units and functions and was extremely comprehensive, including the following:

- Reducing procurement spending through increased volumes

- Consolidating service locations

- Aligning technological standards and platforms

- Closing some manufacturing sites

- Streamlining corporate functions

- Adopting more efficient processes

- Optimizing the go-to-market approach

- Identifying new avenues of growth

The full program consisted of 350 individual initiatives, organized into nine major work streams and aligned with the overall organization structure to create clear accountabilities and tie the program’s impact directly to financial results. Still, many of the initiatives were complex by nature, so solid planning and rigorous program management and reporting have been critical.

Konecranes also carried out a holistic baseline survey to assess the cultures of the two organizations and define a joint target culture. An extensive cultural development and communications plan featured strongly in the early days of the integration.

The company has reported on its progress to investors as part of its quarterly earnings calls, and two years into the three-year plan, it has hit or exceeded its targets. That performance has earned praise from investors, leading to a share price increase of more than 50% since the acquisition was announced.

Key success factors in this turnaround: The combination of competitors presented a clear opportunity to create value from synergies, but management took the more ambitious approach of using the deal as a catalyst for the combined entity to perform at its full potential. Hitting —and often exceeding—performance targets has led to a dramatic rise in the company’s stock price.

Konecranes used the deal as a catalyst for the combined entity to perform at its full potential.

Coop Norge ranked third in Norway’s competitive and consolidated retail-grocery landscape in 2014, with a 22.7% share. But the company faced a major strategic challenge from its two larger competitors, which were able to use their scale advantages to negotiate favorable prices from suppliers while opening new stores. A smaller player, ICA Norway, was in a more precarious position, with a 2014 operating loss of more than $57 million on revenue of $2.1 billion. An acquisition made sense. In buying ICA, Coop aimed to become the number-two player and so increase economies of scale in procurement and logistics. ICA stores in Norway were a strong strategic fit as well, complementing Coop’s existing locations.

After the acquisition closed, Coop rebranded all ICA supermarkets and discount stores to concentrate on fewer, winning formats and to fully leverage improvements and synergies in areas such as procurement, logistics, and store operations. Coop’s discount brand, Extra, was already showing good momentum in the market, and this was accelerated through the ICA Norway transaction.

The integration and rebranding created pride and momentum internally at ICA, which led to improved growth and financial performance at the acquiring company as well. Coop moved up to second place in the market, generated new economies of scale, and realized 87% of its expected results from synergies within just eight months of the close and 96% after two years. And because the company stayed true to its existing store strategy, it was able to lean on previous experience and maintain its long-term vision. Operating profits rose by approximately $270 million, from a loss of $160 million in 2015 to a profit of $106 million in 2016. Revenue during that period increased by 10.7%, to nearly $6 billion, of which ICA stores and Coop’s existing locations accounted for 7.8 and 2.9 percentage points, respectively.

Coop Norge’s early successes in the integration created strong momentum and a culture of success.

Key success factors in this turnaround: The early successes achieved in the integration created strong momentum and a culture of success, enabling the combined entity to increase both revenue and profits in a highly competitive market.

In the early 2010s, the global shipbuilding industry declined significantly, in part because of a contraction in the demand for ships. That left many shipyards—including the Turku yard, which operated in the sophisticated niche of cruise ships and ferries—in need of cash. When Turku’s owner, STX Finland, verged on insolvency in 2014, the Finnish government (which had a stake in STX) began looking for a new owner. Meyer Werft, a leading European shipbuilder, believed that the Turku shipyard could be operated profitably and bought 70% of the yard in September 2014. As part of the deal, Turku secured two new cruise ship projects. With the orders confirmed, Meyer Werft bought the remaining shares, becoming sole owner.

Renamed Meyer Turku Oy, the company began to integrate the shipyard’s operations and find synergies in development, procurement, and other support functions. Having negotiated up-front for new business, it was able to fill Turku’s production capacity, benefit from increased scale, and begin to boost profitability almost immediately. Critically, the deal helped restore trust among employees, which extended to other important stakeholders such as customers and lenders. Such trust is essential in an industry that hinges on building a small number of very large projects, and it was fostered by Meyer Werft’s delivery on promises right from the start.

Meyer Werft then looked to planning growth in the longer term: increasing capex to boost capacity—and profitability—still further and investing in a new crane, cabin production, and a new steel storage and pretreatment plant while modernizing existing equipment. It also entered into a joint R&D project with the University of Turku to develop more sustainable practices across a ship’s life cycle—from raw materials to manufacturing processes and beyond. And it hired 500 new workers, partially replacing retiring employees, in 2018.

As a result, the company increased revenues from $590 million in 2014 to $970 million in 2017, an annual growth rate of more than 18%. It also increased profit margins to 4% in 2017, up from a loss of 5% in the acquisition year. The company now has a stable order book out to 2024, and productivity continues to climb.

Key success factors in this turnaround: In addition to making operational improvements, Meyer Werft was able to foster trust among employees and customers by delivering on its promises and showing its commitment through long-term investment.

Meyer Werft fostered trust among employees and customers by delivering on its promises.

In early 2013, Office Depot and OfficeMax were in a similar situation: online retailers were threatening their business. They agreed on a merger, with the goal of generating synergies by reducing the cost of goods sold, consolidating support functions to cut overhead, and eliminating redundancies in the distribution and sales units.

Because the two companies were merging as equals—rather than one buying the other— some decisions were difficult to make before the close (for example, which IT system the combined entity would use and where headquarters would be located). But management was able to define synergy targets and begin planning the integration during the six months before the close. The companies also created an integration management office (IMO) that addressed areas that were critical for business continuity, specifying which units would be integrated and which would be left as is.

The IMO created playbooks for 15 integration teams, addressing finance, marketing, the supply chain, and e-commerce operations, and developed a plan for communication, talent management, and change management for the overall effort. It categorized all major decisions into two groups: those that could be made prior to the close (because the steering committee was aligned) and those that couldn’t be made during that period. For decisions in the second category, the IMO laid out the two or three best options to consider. Critically, the IMO’s rigorous plans included timelines for how the businesses would evolve over the first, second, and third years of the merger, helping to align functions and manage interdependencies.

Once the deal closed, all this preparation allowed the two organizations to start the integration process immediately on day one. Within weeks, they had agreed on a leadership team for the combined entity, a headquarters site, and an IT platform. The organization was largely redesigned in just two months—a remarkably rapid effort given that it ultimately affected about 9,000 employees.

Most important, the smooth integration process allowed the companies to be extremely rigorous in capturing more synergies—and doing it faster—than anticipated. For example, they integrated the e-commerce businesses in a way that allowed them to retain most key customers. In the first year after the deal closed, the company captured cost savings close to three times management’s original targets; cost savings of the end-state organization were 50% more. In all, the merger unlocked about $700 million, putting the new company in a much better competitive position.

An extremely rigorous integration plan allowed Office Depot and OfficeMax to exceed cost savings targets.

Key success factors in this turnaround: Office Depot and OfficeMax merged in response to the threat of online competition. An extremely rigorous integration plan allowed the combined business to dramatically exceed its cost savings targets.

Texas-based Vistra Energy operates in 12 US states and delivers energy to nearly 3 million customers, with a mix of natural gas, coal, nuclear, and solar facilities enabling about 41,000 megawatts of generation capacity. It was formed in October 2016 when its predecessor emerged from a protracted bankruptcy process.

At the conclusion of bankruptcy proceedings, Vistra underwent a corporate restructuring, moving from a siloed operating model to a unified organization with a centralized leadership team and common objectives. New governance structures facilitated more consistent and rigorous corporate decision making, with an emphasis on capital allocation and risk management. In addition, management immediately launched a turnaround effort to reduce costs and improve performance across the entire organization.

In all, the company managed to reduce costs and enhance EBITDA by approximately $400 million per year, exceeding its original target by $40 million without any drop in service levels or safety standards. At the same time, investments in new service offerings—many enabled by digital technology—boosted customer satisfaction.

In 2017, Vistra announced the acquisition of Dynegy, one of its largest peers, resulting in the largest competitive integrated power company in the US. The combined entity offers significant synergies, with Vistra now on track to deliver $500 million of additional EBITDA per year, along with annual after-tax free cash flow benefits of nearly $300 million and $1.7 billion in tax savings. The deal also allows Vistra to expand into new US markets, diversifying its operations and earnings, reducing its overall business risk, and creating a platform for future growth.

The addition of Dynegy also supports Vistra’s shift toward a more modern power generation fleet based on natural gas. The company preceded that deal with the acquisition of a large, gas-fueled power plant in west Texas, and it also retired several uneconomical coal-burning facilities. In all, Vistra’s generation profile has evolved from approximately two-thirds coal-fueled sources to more than 50% natural gas and renewables.

With these measures—a successful turnaround followed by two strategic acquisitions—Vistra has positioned itself to sustainably create value for its shareholders in a very competitive industry.

Key success factors in this turnaround: Vistra’s acquisition of Dynegy represented both a pivot to growth and an opportunity to extend cost savings to an acquired operating platform.

Managing Director & Partner

Managing Director & Senior Partner; Global Leader, BCG Transform Practice

Project Leader

Partner & Director, Change, Transaction & Integration Excellence

Managing Director & Senior Partner; Global Leader of Transactions & Integrations

Los Angeles

Managing Director & Senior Partner

ABOUT BOSTON CONSULTING GROUP

Boston Consulting Group partners with leaders in business and society to tackle their most important challenges and capture their greatest opportunities. BCG was the pioneer in business strategy when it was founded in 1963. Today, we work closely with clients to embrace a transformational approach aimed at benefiting all stakeholders—empowering organizations to grow, build sustainable competitive advantage, and drive positive societal impact.

Our diverse, global teams bring deep industry and functional expertise and a range of perspectives that question the status quo and spark change. BCG delivers solutions through leading-edge management consulting, technology and design, and corporate and digital ventures. We work in a uniquely collaborative model across the firm and throughout all levels of the client organization, fueled by the goal of helping our clients thrive and enabling them to make the world a better place.

© Boston Consulting Group 2024. All rights reserved.

For information or permission to reprint, please contact BCG at [email protected] . To find the latest BCG content and register to receive e-alerts on this topic or others, please visit bcg.com . Follow Boston Consulting Group on Facebook and X (formerly Twitter) .

Subscribe to our M&A, Transactions, and PMI E-Alert.

Case Studies of Successful Mergers

MergerAcquisition.io

Welcome to our exploration of successful mergers through the lens of compelling case studies. We'll delve into the strategies, execution, and outcomes that have defined some of the most successful corporate mergers in recent history. These case studies will not only provide insights into the complexities of mergers but also shed light on the factors that contribute to their success.

The Power of Mergers: An Overview

Mergers represent a significant shift in the business landscape. They can transform industries, redefine market leaders, and create new opportunities for growth. However, the path to a successful merger is often fraught with challenges. It requires strategic planning, careful execution, and a clear vision of the desired outcome.

In this section, we will explore the concept of mergers, their potential benefits, and the factors that contribute to their success. We will also touch upon the importance of studying case studies to understand the dynamics of successful mergers.

Case Study 1: The Disney-Pixar Merger

The merger between Disney and Pixar in 2006 is a classic example of a successful merger. The two companies had a long-standing relationship, with Pixar creating some of the most successful films for Disney. However, the merger took this relationship to a new level, creating a powerhouse in the animation industry.

The success of this merger can be attributed to several factors. Firstly, the merger was based on mutual respect and a shared vision for the future. Secondly, the merger allowed Pixar to retain its unique culture and creative process, which was crucial to its success. Lastly, the merger resulted in a series of successful films, which further cemented the partnership between the two companies.

Case Study 2: The Exxon-Mobil Merger

The merger between Exxon and Mobil in 1999 is another example of a successful merger. This merger created the largest company in the world at the time, with a combined market value of over $80 billion.

The success of this merger can be attributed to the complementary strengths of the two companies. Exxon had a strong presence in the Middle East and Asia, while Mobil had a strong presence in Europe and Africa. The merger allowed the combined company to leverage these strengths and expand its global reach.

Case Study 3: The Vodafone-Mannesmann Merger

The merger between Vodafone and Mannesmann in 2000 is considered one of the most successful mergers in the telecommunications industry. The merger created the largest mobile telecommunications company in the world, with over 42 million customers.

The success of this merger can be attributed to the strategic fit between the two companies. Vodafone was a leader in the mobile telecommunications market, while Mannesmann had a strong presence in the fixed-line telecommunications market. The merger allowed the combined company to offer a comprehensive range of telecommunications services.

Case Study 4: The Procter & Gamble-Gillette Merger

The merger between Procter & Gamble and Gillette in 2005 is a prime example of a successful merger in the consumer goods industry. The merger created a company with a combined revenue of over $60 billion.

The success of this merger can be attributed to the complementary product portfolios of the two companies. Procter & Gamble was a leader in the household goods market, while Gillette was a leader in the personal care market. The merger allowed the combined company to offer a wider range of products to consumers.

Lessons from Successful Mergers

Studying these case studies provides valuable insights into the factors that contribute to the success of mergers. These factors include a shared vision, complementary strengths, strategic fit, and respect for the unique culture of each company.

However, it's important to note that each merger is unique and what works for one may not work for another. Therefore, it's crucial to carefully analyze each situation and develop a tailored strategy for success.

Wrapping Up: Gleaning Insights from Successful Mergers

As we wrap up our exploration of successful mergers, it's clear that these case studies offer valuable insights for businesses considering a merger. They highlight the importance of strategic planning, mutual respect, and a shared vision for success. While each merger is unique, these case studies provide a roadmap for navigating the complexities of mergers and achieving success.

- Browse All Articles

- Newsletter Sign-Up

Acquisition →

- 20 Jun 2023

- Cold Call Podcast

Elon Musk’s Twitter Takeover: Lessons in Strategic Change

In late October 2022, Elon Musk officially took Twitter private and became the company’s majority shareholder, finally ending a months-long acquisition saga. He appointed himself CEO and brought in his own team to clean house. Musk needed to take decisive steps to succeed against the major opposition to his leadership from both inside and outside the company. Twitter employees circulated an open letter protesting expected layoffs, advertising agencies advised their clients to pause spending on Twitter, and EU officials considered a broader Twitter ban. What short-term actions should Musk take to stabilize the situation, and how should he approach long-term strategy to turn around Twitter? Harvard Business School assistant professor Andy Wu and co-author Goran Calic, associate professor at McMaster University’s DeGroote School of Business, discuss Twitter as a microcosm for the future of media and information in their case, “Twitter Turnaround and Elon Musk.”

- 29 Nov 2022

- Research & Ideas

Is There a Method to Musk’s Madness on Twitter?

Elon Musk's brash management style has upended the social media platform, but was bold action necessary to address serious problems? Andy Wu discusses the tech entrepreneur's takeover of Twitter.

- 13 Dec 2021

The Unlikely Upside of Mergers: More Diverse Management Teams

Mergers shake up the status quo at companies and help women and people of color move up the ladder. Research by Letian Zhang mines data from 37,000 deals. Open for comment; 0 Comments.

- 14 Jan 2021

- Working Paper Summaries

Dog Eat Dog: Measuring Network Effects Using a Digital Platform Merger

With heated debate over antitrust regulation of online platforms, this study finds that when a larger platform acquired its greatest competitor, users were not better off with a single platform compared with two competitors, despite marked efficiency improvements experienced by the acquiring platform.

- 30 Nov 2020

Short-Termism, Shareholder Payouts, and Investment in the EU

Shareholder-driven “short-termism,” as evidenced by increasing payouts to shareholders, is said to impede long-term investment in EU public firms. But a deep dive into the data reveals a different story.

- 26 Jun 2020

Weak Credit Covenants

Prior to the 2020 pandemic, the leveraged loan market experienced an unprecedented boom, which came hand in hand with significant changes in contracting terms. This study presents large-sample evidence of what constitutes contractual weakness from the creditors’ perspective.

- 13 Jan 2020

Do Private Equity Buyouts Get a Bad Rap?

Elizabeth Warren calls private equity buyouts "Wall Street looting," but a recent study by Josh Lerner and colleagues shows they have both positive and negative impacts. Open for comment; 0 Comments.

- 05 Nov 2019

The Economic Effects of Private Equity Buyouts

Private equity buyouts are a major financial enterprise that critics see as dominated by rent-seeking activities with little in the way of societal benefits. This study of 6,000 US buyouts between 1980 and 2013 finds that the real side effects of buyouts on target firms and their workers vary greatly by deal type and market conditions.

- 21 Aug 2019

Improving Customer Compatibility with Operational Transparency

Service firms seeking prospective customers usually highlight the advantages of their offerings and downplay the tradeoffs. This study suggests a different approach: Provide transparency into advantages as well as tradeoffs. The transparency helps customers make informed decisions and can lead to better outcomes for both firms and customers over the long run.

- 05 Jun 2019

If Your Customers Don't Care What You Charge, What Should You Charge?

Consumer inertia is the tendency of some customers to buy a product, even when superior options exist. Alexander J. MacKay discusses how that habit affects competitive strategy and even regulatory oversight. Open for comment; 0 Comments.

- 04 Jun 2019

Political Influence and Merger Antitrust Reviews

This paper uses a large sample of United States mergers between 1998 and 2010 to study how political connections help firms obtain favorable antitrust regulatory outcomes for mergers. Given that antitrust regulators are subject to congressional oversight, the authors predict and find evidence that outcomes systematically favor firms that are constituents of politicians serving on judiciary committees.

- 30 May 2019

US Antitrust Law and Policy in Historical Perspective

Since the late 19th century, American antitrust law and policy has responded to multiple changes: technological advances that have transformed business structures, political imperatives that have reformed regulations and informed prosecutorial discretion, and economic theories that have reshaped the boundaries of government interventions into the economy. Today, antitrust remains a contested field.

- 10 Apr 2019

Trade Secrets Protection and Antitakeover Provisions

The study examines managers’ responses when facing an increased threat of their firm being acquired. Results add to our knowledge of the use of antitakeover provisions, showing that managers, particularly in high-innovation firms, increase certain provisions to protect long-term innovation output in the presence of elevated acquisition risk.

- 14 May 2018

Amazon vs. Whole Foods: When Cultures Collide

Amazon's acquisition of Whole Foods seemed a Wall Street dream come true. But then Amazon's data-driven efficiency met the customer-driven culture at Whole Foods—and the shelves began to empty. Dennis Campbell and Tatiana Sandino discuss their new case study. Open for comment; 0 Comments.

- 12 Feb 2018

Private Equity, Jobs, and Productivity: Reply to Ayash and Rastad

In 2014, the authors published an influential analysis of private equity buyouts in the American Economic Review. Recently, economists Brian Ayash and Mahdi Rastad have challenged the accuracy of those findings. This new paper responds point by point to their critique, contending that it reflects a misunderstanding of the data and methodology behind the original study.

- 25 Jan 2016

When Negotiating a Price, Never Bid with a Round Number

Investors who offer “precise” bids for company shares yield better outcomes than those who offer round-number bids, according to research by Petri Hukkanen and Matti Keloharju. Open for comment; 0 Comments.

- 03 Sep 2009

- What Do You Think?

Are Retention Bonuses Worth the Investment?

There is a time and place for retention bonuses but they should be used sparingly, wrote many respondents to this month's column, says Professor Jim Heskett. Others challenged the value of bonuses, and suggested compelling alternatives. (Online forum now closed; next forum begins October 2.) Closed for comment; 0 Comments.

- 15 Dec 2008

The Surprisingly Successful Marriages of Multinationals and Social Brands

What happens when small iconic brands associated with social values—think Ben & Jerry's—are acquired by large concerns—think Unilever? Can the marriage of a virtuous mouse and a wealthy elephant work to the benefit of both? Professors James E. Austin and Herman B. "Dutch" Leonard discuss their research. Closed for comment; 0 Comments.

- 28 Nov 2005

Unilever: Transformation and Tradition

In a new book, professor Geoffrey Jones looks at Unilever's decades-old transformation from fragmented underperformer to focused consumer products giant. This epilogue summarizes the years 1960 to 1990. Closed for comment; 0 Comments.

- 02 Apr 2001

Not All M&As Are Alike—and That Matters

In this Harvard Business Review article, Professor Joseph L. Bower shares some of the results of his year-long study of M&A activity sponsored by HBS. Discover how five distinct merger and acquisition strategies scenarios play out—and his recommendations for success. Closed for comment; 0 Comments.

Realizing M&A value creation in US banking and fintech: Nine steps for success

Co-leads McKinsey’s Global Banking & Securities Practice and our work in North America. Ishaan works with clients across financial services and private equity. His client service spans strategy, corporate finance, digital and analytics, performance transformation, and M&A.

Advises financial institutions on capital markets, valuation, investor communications, and strategy topics

Serves leading financial institutions on strategy and M&A throughout the deal cycle – from due diligence through integration. He co-leads McKinsey's banking M&A joint venture globally. Max also works intensively with fintechs and leads the Fintech Practice in Germany

Advises executives across industries on mergers and acquisitions—including mergers, integrations, alliances, and divestitures—bringing particular expertise in strategy and performance in the pharmaceuticals and medical-products sector

Leads McKinsey’s Global M&A and Banking/Fintech service line, with extensive experience in counseling senior executives on and leading due diligence and integrations in FIG, Fintech and TMT sectors

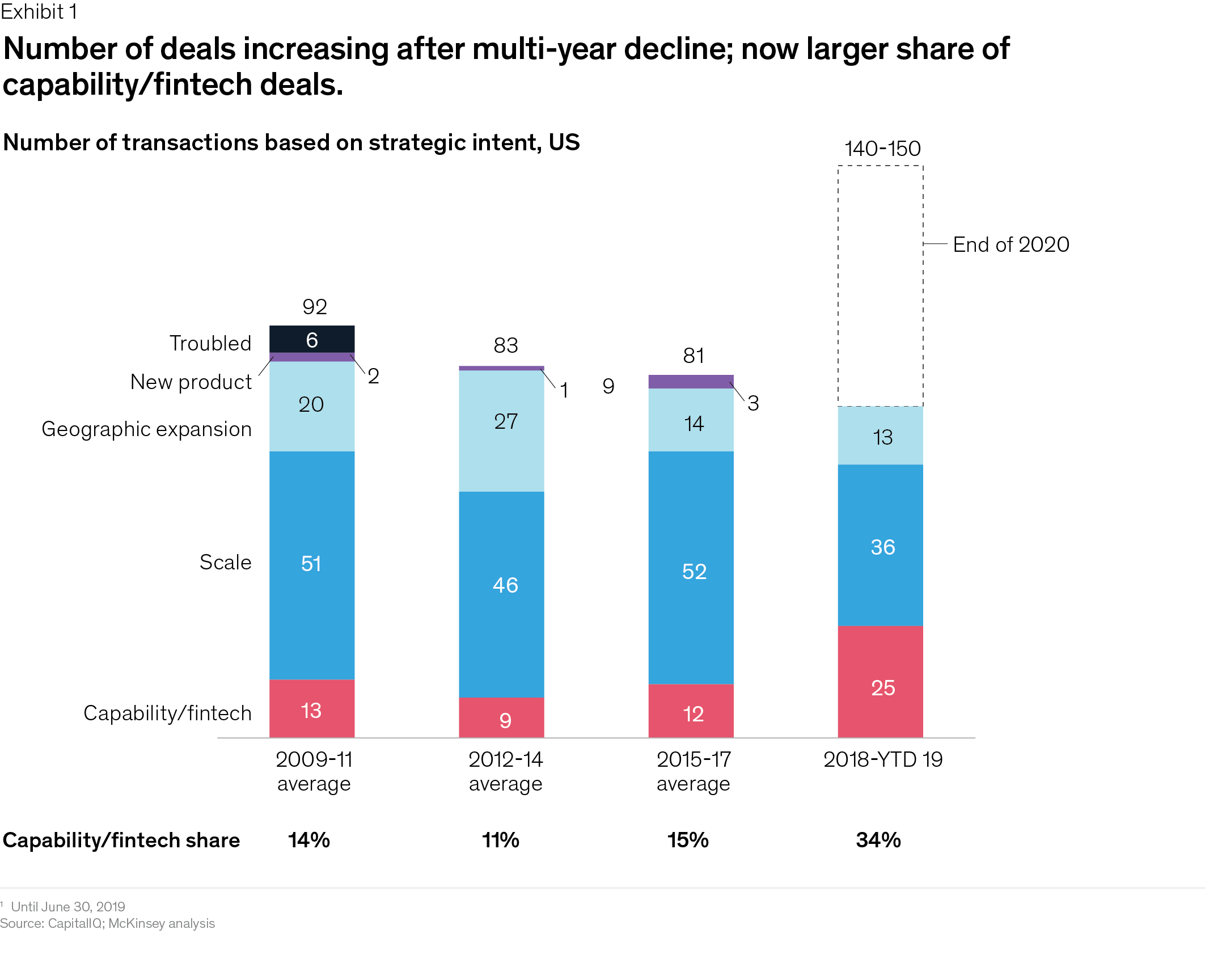

November 15, 2019 For almost a decade after the financial crisis, M&A activity in the US banking industry remained limited, as many banks wrestled with challenging integrations and “shot-gun” combinations. But deal-making bounced back in 2018 and looks likely to expand. While several factors favor that growth, would-be deal-makers face obstacles. Our analysis suggests that most US bank mergers from that decade failed to create value. Going forward, US banks will require a smart strategy and the right integration approach to fully realize the value creation potential in M&A.

US banking M&A is on the upswing

US banking M&A was relatively flat from 2009 to 2017; the industry averaged about 20 deals a year. But in 2018 activity more than doubled, as US banks completed 49 transactions. And, with total deal value of $38 billion through the first half of 2019, this year already substantially outpaces 2018.

While many recent deals, such as the merger of BB&T and SunTrust and that of TCF and Chemical Financial, have focused on increasing geographic footprints and scale efficiencies, 1,2 fintech and capability-building deals are gaining traction. US banks averaged just three or four fintech deals per year through 2017, but deal volume exploded in 2018 with 16 transactions, and the first half of 2019 saw nine fintech deals (Exhibit 1). A good example of recent deals is Goldman Sachs’ acquisition of United Capital and its FinLife CX digital customer-service platform to add an advisor-led tech-enabled platform to the bank’s growing suite of digital offerings. 3

Tailwinds favor M&A growth

In 2019, market reaction to bank-to-bank and fintech mergers has generally been positive. On the day of deal announcement, the market rewarded both BB&T and SunTrust with share value increases of 4 percent and 10 percent, respectively. More fundamentally, we believe there are multiple reasons why M&A activity in US banking could continue to increase.

The profitability of US banks has improved substantially, thanks to significant productivity investments, higher interest rates, and lower taxes. The average ROE of US banks climbed from 8.6 percent in 2013 to 10.8 percent in 2018. Banks also enjoy a stronger capital position that puts them in a better position to execute M&A.

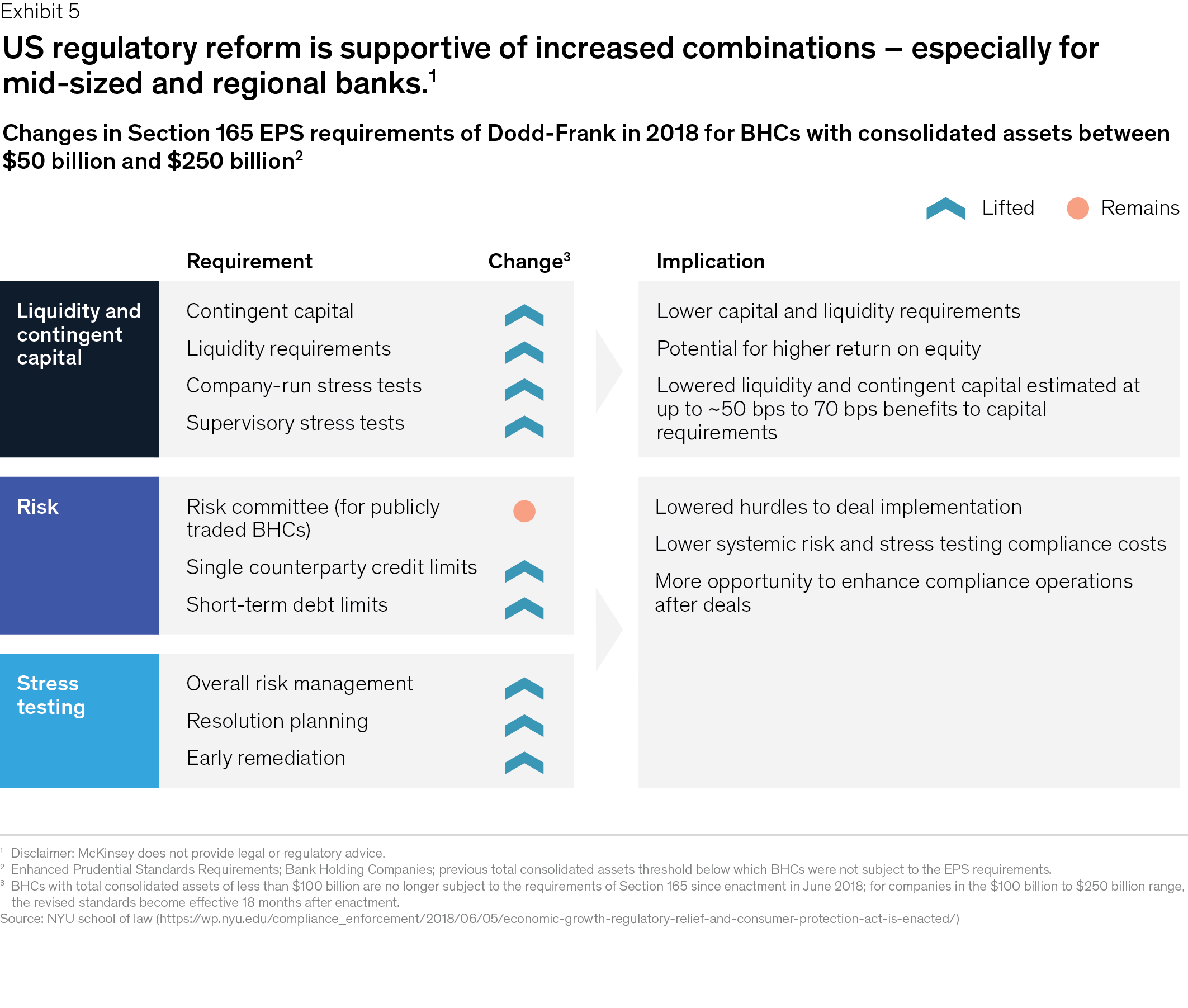

Regulatory reform is reducing requirements for banking combinations. The threshold triggering substantial additional process and capital measures has increased from $50 billion to $250 billion (Exhibit 5). This particularly benefits regional banks that need greater size and scale to strengthen their competitive position for deposits versus larger banks—where they have been challenged.

US regional banks face intense pressure to build new capabilities in robotics, machine learning/artificial intelligence, and advanced analytics (e.g., people and talent analytics) as banking increasingly digitizes. M&A is one of the best ways to acquire skills or generate cost efficiencies that can fund internal efforts. For example, when BB&T acquired SunTrust, it announced a cost-savings target of $1.6 billion and plans to invest a substantial portion into digital banking. 5 JPMorgan Chase earmarked $11.5 billion in 2019 alone for technology investments, with machine learning, artificial intelligence and blockchain identified as top priorities; a good example is the bank’s recent acquisition of InstaMed, to support its position in payments. CapitalOne purchased Wikibuy, an online website that allows shoppers to compare prices for items, to help customers “feel confident in their purchasing decisions.” 6

The US is home to a lot of banks. While consolidation has steadily reduced the number of US banks from roughly 15,000 in 1985 to about 5,000 today, many industry executives and experts expect the consolidation trend to continue. Our research shows that more than 60 US banks with assets of $10 billion to $25 billion might be attractive acquisition targets for well-positioned regional banks—for example, regional banks with a high cost-income ratio and a low loans-to-deposits ratio, among other factors.

Beyond these trends favoring M&A growth, we believe that M&A will prove critical to next-generation transformation in US banking. Leading digital European markets clearly demonstrate the power of digitized banking, as banks there are achieving cost-to-asset ratios as much as 60 to 80 percent lower than US banks. A smart, well-executed M&A strategy can equip US banks to make slow internal efforts history. Banks can dramatically improve their cost productivity, with machine learning and robotics, and their people development, with advanced people analytics that better match talent to value and develop future leaders.

Successful bank acquirers get nine things right

In our experience, successful bank acquirers of other banks and fintechs take a strategic, long-term approach to M&A. They invest time and resources to build an end-to-end M&A approach, including deep understanding of how M&A serves their overall strategy, optimal candidate development and cultivation approaches, the merger management expertise required to execute, and the long-term capability development that enables them to deliver consistently. In our work, we see the most effective acquirers apply nine principles to realize full value from their M&A strategy.

1. Make M&A a core plank of the overall strategy—don’t rely on opportunistic M&A.

Too many acquirers resort to M&A as a way to buy growth or acquire an asset opportunistically, reacting to available deal flow to drive activity, without thorough understanding of how the deal will create value.

The best acquirers embed M&A in their strategic planning process. They require businesses to identify where inorganic moves are necessary to advance the bank’s strategy and then translate these moves into actionable deal theses that guide candidate scanning, prioritization, and progress review. Only after pressure-testing and prioritizing these themes do leaders develop lists of M&A targets that fit the investment themes within the overall strategy.

For banks, this means making M&A an integral part of the capital-planning process, with the annual capital plan adjusted—materially—to support the highest-potential investment themes. Practically speaking, this effort requires getting very clear on the decision rights and governance model for M&A execution; for example, who leads pre-diligence exploration of companies on the M&A candidate lists, what role the CFO plays, and what triggers full diligence.

2. Continuously cultivate top-priority deal candidates with a programmatic approach, not one-off efforts.

The best bank acquirers source and develop potential M&A candidates continuously and develop them across all stages of the M&A process. These efforts extend from conducting rapid pre-diligence review of prioritized targets, including high-level valuation and assessment of synergy potential, to proactive outreach to targets, supported by talking points on the bank’s partnership vision.

3. Assess the full spectrum of opportunities, including partnerships, joint ventures, and alliances, to gain scale and capabilities.

Highly innovative industries like pharmaceuticals and high-tech have long relied on joint ventures and alliances to develop their businesses. As banking advances further into digitization and advanced analytics, JVs and alliances are becoming much more relevant, especially for regional banks that lack the digital and fintech M&A resources of the larger money center banks. In particular, to succeed in digitization, many regional banks will have to assess the full range of partnership opportunities, from full joint ventures (with or without equity) to strategic partnerships to contractual alliances.

4. Tap divestitures to strengthen value creation—don’t buy without understanding the potential for a simultaneous sale.

Our analysis of thousands of deals finds that companies active in divesting, not just acquiring, achieve TRS that is 1.5 to 4.7 percent higher than the TRS of companies focused on acquisitions alone.

Successful bank acquirers use forcing mechanisms like the budget process to review the landscape of potential assets to sell and proactively shape the assets for sale based on an understanding of their value to a more natural owner. These winners also pay special attention to managing the stranded costs that can represent huge value leaks for banks.

One leading money center bank makes divestiture review part of its annual strategic planning process, evaluating businesses throughout the year on their strategic importance, operational value, and amount of capital freed up, if sold. The bank has a “productivity czar” who reports to the CEO and uses an algorithm-supported approach to counter the tendency of division leaders to protect assets in their portfolio by overstating their importance. The algorithm deepens insight into growth contribution (or lack of), required management resources, operational complexity, capital deployed, and ROE impact. This approach makes the bank much more nimble in divestitures and ready to use “acquisitions for growth” as catalysts for simultaneous value-adding divestitures.

5. Establish a value-added integration management office (IMO) led by an “integration CEO”—don’t make integration a checklist exercise.

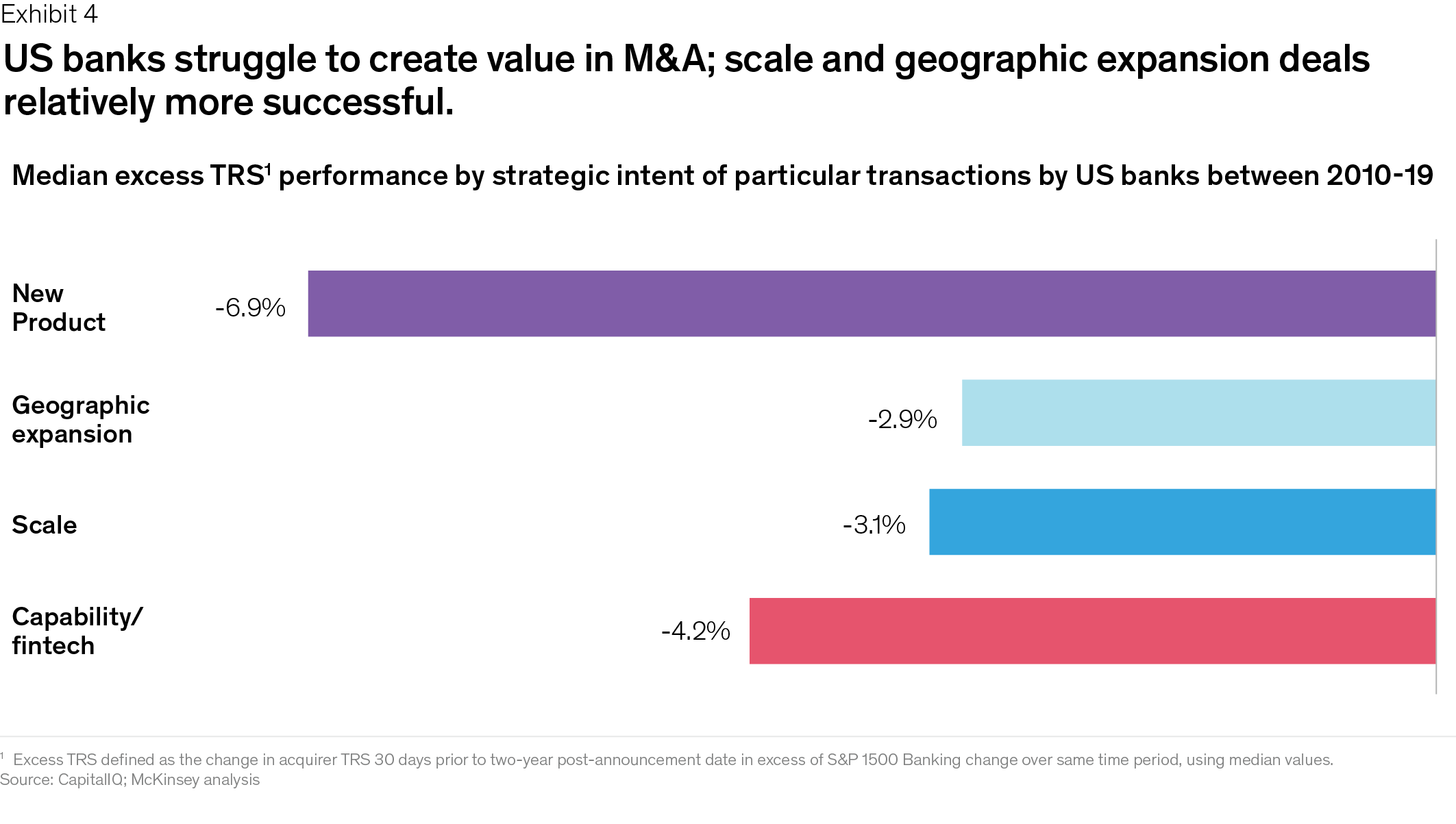

We often hear financial industry executives say that they have a merger playbook and know how to execute. But the TRS numbers show that banks have struggled to create value through M&A.

Beating the odds requires more than checklists used in past integrations or third-party process support. M&A winners establish an IMO and empower an integration CEO to tailor how they manage every integration effort to deal rationale and sources of value. For example, winners heavily discount cost synergies envisioned beyond 24 to 30 months because they know the importance of realizing the lion’s share of the synergies in year one. Winners also move purposefully to take control of the acquired bank, particularly its credit decisions, portfolio management, and back-office systems and costs. One leading bank mobilized a “SWAT” team to stabilize the target’s shaky balance sheet and free up substantial capital. Winners also implement cost-saving measures as soon as possible. Failure to do so poisoned the culture in one bank’s branch sales network through delaying inevitable branch headcount reductions until several months into the integration effort.

6. “Open the aperture” on capturing value—don’t rest with the due diligence numbers.

Failing to update synergy expectations during integration is one of the most common, but avoidable, pitfalls in any transaction. This is especially true in banking, where the industry structure invites treating M&A as a project. This project typically sets synergy targets during due diligence, builds the targets into department operating budgets, and creates a checklist-based PMO process to monitor progress against the targets.

M&A winners regularly exceed due diligence synergy estimates by 200 to 300 percent because they reassess synergy potential throughout the life cycle of the deal, especially pre-close, pushing hard to uncover upside and transformational synergies. In successful banking deals, this often means dividing synergy-capture efforts into two time-based categories ─ initiatives that move quickly to generate maximum bottom-line impact in the first year (and often capture 50 to 70 percent of the cost synergies) and larger, longer-term initiatives that are typically technology-dependent.

Protecting the base business is a critical component of value capture that often goes unappreciated in banking mergers. M&A leaders make taking frequent temperature checks and attending to the health of the front-line business and customer satisfaction during integration a core responsibility of the integration CEO. For example, customer churn in corporate banking requires special attention early in the merger, since many customers do business with multiple banks. In a recent successful merger, this meant proactive outreach to corporate customers by pairs of acquirer/target relationship managers and careful manual migration of customers to the acquiring bank to avoid any errors or complaints.

Ensuring that the value capture team opens the aperture on synergies is particularly important given the recent tendency to announce a banking deal as a “merger of equals.” The intent is admirable but impractical to enact. Merger-of-equals positioning may benefit pricing, but it typically slows and softens decision-making, hamstrings implementation, and raises the risk of value leakages throughout the integration effort.

7. Build an independent technology roadmap—don’t let current business operators and maintenance dictate the approach to capturing value.

In our experience, IT enables about 70 percent of a bank’s cost synergies but, without careful planning, can easily take 50 percent longer than expected to capture the value and can add incremental costs of 50 to 100 percent to what the bank already spends on IT. Making tough choices on IT integration is especially challenging for banks because they rely heavily on third parties to maintain their many custom-built legacy platforms. Banks can’t always count on those providers to provide objective advice on the right technology roadmap to follow.

Successful bank acquirers make IT integration a strategic priority, rather than a PMO-managed integration project. They develop an overall technology blueprint aligned with their strategy, sources of deal value, and customer-service requirements before launching costly IT integration initiatives and project management. One M&A leader looks to independent, internal subject-matter experts to build the “no case” for proposed technology roadmaps, tasking them with pressure-testing the logic and forcing discussion of other options.

This approach is particularly salient in fintech deals, since, along with talent, the technology platform is often the raison d’être of the deal, but in some cases that platform may meaningfully exceed the experience and expertise of the bank’s IT team. The bank must determine as early as possible what capabilities of the target the deal should preserve and what target-specific attributes (people, processes, and platforms) make those capabilities work so the integration effort can protect and nurture those attributes to scale.

One M&A leader has repeatedly chosen its future platform within the first months after deal announcement, using workarounds after close to maintain an adequate customer experience until the optimal systems integration roadmap is ready. This bank often migrates first and transforms later because it knows that advancing on both fronts at once is too complex. In a recent successful bank-fintech merger, customer migration proceeded in two waves—manual migration of corporate customers, followed by automated migration of retail customers. Goldman Sachs’ acquisition of Final is a good example of a deal that augments strategy, in particular Goldman Sachs’ publicly stated objective to invest in its consumer-centric business. Final impacts Goldman Sachs’ partnership with Apple Card by adding digital features for fraud and theft protection, including those which allow consumers to monitor their spending in real time.

8. Take a scientific approach to identifying cultural issues and change management—don’t pay lip service to cultural integration.

Mission, vision, and values can look very similar across banks. Executives often return from pre-deal announcements convinced that the cultures of the companies involved are very similar and that smooth organizational integration will be a snap. This is a major source of deal failure. M&A leaders don’t underestimate the importance of proactively tackling the challenges involved in integrating cultures. They understand that culture goes beyond values and comes alive in a company’s management practices—the way that work gets done, such as whether decisions are made by consensus or by the most senior accountable executive.

If not addressed properly, cultural integration challenges inevitably lead to friction among leaders, decreased productivity, increased talent attrition, and lost value. M&A leaders rigorously assess top management practices and working norms early and design the overall program to align practices and mitigate risks early and often. Alphabet, for example, is well-known for a programmatic approach to M&A and integration of fintech acquisitions that proceeds in phases linked to talent and sources of deal value.

Successful cultural integration often lends itself to an added area of opportunity in scale mergers. In these cases, the merger itself can be leveraged to reinforce critical behaviors that may be lacking in the acquiring organization, thereby creating not just an integrated culture but putting a stop to bad behaviors that might have existed pre-integration. In these situations, leading organizations choose to evaluate culture, and more broadly talent management and experience, holistically across both organizations and set a clear aspiration for a merged culture that will best enable the new organization’s strategic goals. This is particularly important when the acquisition brings in fundamentally new talent pools that may have different definitions of success, progression, and experience, as in the acquisition of a fintech into a large traditional bank.

M&A leaders also don’t skimp on formal change management planning. They take a rigorous and regimented approach to each phase of the integration, engaging stakeholders through the process and ensuring a dedicated handoff period for the transition to steady state.

9. Build capabilities for future deals—take full advantage of every opportunity to deepen the bench.

M&A leaders treat each deal as an opportunity to upgrade their M&A team’s skills and expertise. In banking M&A, talent is increasingly emerging as one of the primary sources of competitive advantage. Banks that allocate human capital, as well as financial resources, strategically and dynamically stand to generate significant economic return. This makes leadership and talent development the “next big thing” for unlocking value in banking M&A, with direct impact on the bottom line. After doing a deal, M&A leaders are just as rigorous in measuring success. They carefully track deal impact across critical KPIs, such as lower cost-income ratios, increased revenue growth above base trajectory, and more efficient use of capital.

Many CEOs and top teams in US banking and fintech see increasing their existing talent bench as critical for success, as has been raised with McKinsey in multiple CEO discussions and recent banking executive roundtables. Most need to make building M&A and integration skills a top priority. This calls for defining their talent development needs comprehensively and responding appropriately—for example, with executive training programs, leadership development, functional capability-building, coaching, and proprietary diagnostics for the talent development “playbook.”

One winning financial industry acquirer regularly devotes a full day, usually a weekend, to reviewing the profiles needed for the integration of a specific deal. This M&A leader spends substantial time identifying the right talent for each role and making sure that the hand-picked leaders get the right training to succeed in the context of the given deal.

Deal-making by US banks spiked in 2018 and shows an upward trajectory for 2019. Many banks can capitalize on the opportunities, especially if they apply the principles of M&A strategy and integration that have served the few successful acquirers in the industry so well.

The authors would like to acknowledge the contributions of Alok Bothra, Alex Camp, Kameron Kordestani, Steve Miller, and Zoltan Pinter to this article.

1 “BB&T and SunTrust to Combine in Merger of Equals to Create the Premier Financial Institution,” SunTrust press release, February 7, 2019.

2 “Chemical Financial Corporation and TCF Financial Corporation Close Merger of Equals to Become the New TCF,” Business Wire, August 1, 2019.

3 “Why United Capital Chose Goldman, Not a PE Backer,” Barrons, May 16, 2019.

4 Based on comparison with an index of peers’ TRS during the two years following an acquisition.

5 “BB&T and SunTrust to Combine in Merger of Equals to Create the Premier Financial Institution,” SunTrust press release, February 7, 2019.

6 “Changing the Game: Saving Money Online Is Easy, Lightning Fast With Wikibuy from Capital One,” CapitalOne.com.

7 “U.S. Bank expands fintech partnerships to B2B space,” usbank.com, October 29, 2018.

- SUGGESTED TOPICS

- The Magazine

- Newsletters

- Managing Yourself

- Managing Teams

- Work-life Balance

- The Big Idea

- Data & Visuals

- Reading Lists

- Case Selections

- HBR Learning

- Topic Feeds

- Account Settings

- Email Preferences

The Case for M&A in a Downturn

- Brian Salsberg

Companies that made significant acquisitions during the financial crisis outperformed those who didn’t.

As companies begin planning for a post-Covid future, there may be opportunities to make one or more long-sought acquisitions. Deal premiums are likely to come down and assets that companies had been reluctant to sell may become available. But the window for maximizing value could be relatively short, if history is any indication. An analysis of evidence from the global financial crisis shows that companies that made significant acquisitions outperformed those that did not. Companies considering an M&A will need to consider some of the unique aspects to getting a deal done, from transaction diligence to post-acquisition integration.

In these difficult times, we’ve made a number of our coronavirus articles free for all readers. To get all of HBR’s content delivered to your inbox, sign up for the Daily Alert newsletter.

Most companies are still in the early days of assessing the impact from the Covid-19 crisis on their business. But as they begin planning for the future, there may be opportunities to make one or more long-sought acquisitions.

- Brian Salsberg is the EY Global Buy and Integrate Leader. In this role, he leads fully-integrated M&A management services across sectors for the EY organization. He has experience working directly with CEOs, executives, business teams and boards of directors, as well as PE-backed companies, in all facets of strategic planning, due diligence, corporate development and M&A.

Partner Center

Mastering M&A: Your Ultimate Guide for Understanding Mergers and Acquisitions

- August 11, 2023

Table of Contents

The process of two companies or their major business assets consolidating together is known as an M&A (merger and acquisition). It is a business strategy involving two or more companies merging to form a single entity or one company acquiring another. These transactions take place entirely on the basis of strategic objectives like market growth, expanding the company’s market share, cost optimisation and the like.

M&As are also an essential component of investment banking capital markets . It helps in revenue generation, shaping market dynamics, and more. This article will provide a profound understanding of mergers and acquisitions including the types, processes, and various other nitty-gritty involved in the investment banking fundamentals relevant to this business strategy .

Types of Mergers and Acquisitions

There are many types associated with the mergers and acquisitions strategy. These are:

Horizontal Mergers

The merger or consolidation of businesses between firms from one industry is known as a horizontal merger. This occurs when competition is high among companies operating in the same domain. Horizontal mergers help companies gain a higher ground due to potential gains in market share and synergies. Investment banking firms have a major role to play in identifying potential partners for this type of merger.

Vertical Mergers

A vertical merger occurs between two or more companies offering different supply chain functions for a particular type of goods or service. This form of merger takes place to enhance the production and cost efficiency of companies specialising in different domains of the supply chain industry. Investment banking firms help in the evaluation of said synergies to optimise overall operational efficiency.

Conglomerate Mergers

A conglomerate merger occurs when one corporation merges with another corporation operating in an entirely different industry and market space. The very term ‘conglomerate’ is used to describe on company related to several different businesses.

Friendly vs. Hostile Takeovers

Leveraged buyouts (lbos) .

A leveraged buyout occurs when a company is purchased via two transactional forms, namely, equity and debt. The funds of this purchase are usually supported by the existing or in-hand capital of a company, the buyer’s purchase of the new equity and funds borrowed.

Investment banking services are majorly relied upon throughout the entire process encompassing a leveraged buyout. Investment banking skills are necessary for supporting both sides during a bid in order to raise capital and or decide the appropriate valuation.

Mergers and Acquisitions Process

To succeed in investment banking careers, your foundational knowledge in handling mergers and acquisitions (M&A) should be strong. Guiding clients throughout the processes involved in M&A transactions is one of the core investment banking skills.

Preparing for Mergers and Acquisitions

To build a strong acquisition strategy, you need to understand the specific benefits the acquirer aims to gain from the acquisition. It can include expanding product lines or entering new markets.

Target Identification and Screening

The acquirer defines the requirements involved in identifying target companies. They may include criteria like profit margins, location, or target customer base. They use these criteria to search for and evaluate potential targets.

Due Diligence

The due diligence process begins after accepting an offer. A comprehensive examination is conducted wherein all aspects of the target company's operations are analysed. They may include financial metrics, assets and liabilities, customers, and the like. Confirming or adjusting the acquirer's assessment of the target company's valuation is the main goal.

Valuation Methods

Assuming positive initial discussions, the acquirer requests detailed information from the target company, such as current financials, to further evaluate its suitability as an acquisition target and as a standalone business.

Negotiating Deal Terms

After creating several valuation models, the acquirer should have enough information to make a reasonable offer. Once the initial offer is presented, both companies can negotiate the terms of the deal in more detail.

Financing M&A Transactions

Upon completing due diligence without significant issues, the next step is to finalise the sale contract. The parties decide on the type of purchase agreement, whether it involves buying assets or shares. While financing options are usually explored earlier, the specific details of financing are typically sorted out after signing the purchase and sale agreement.

Post-Merger Integration

Once the acquisition deal is closed, the management teams of the acquiring and target companies cooperate together to merge the two firms and further implement their operations.

Taking up professional investment banking courses can help you get easy access to investment banking internships that will give you the required industry-level skills you need to flourish in this field.

Financial Analysis

Financial statements analysis .

Financial statement analysis of a merger and acquisition involves evaluating the financial statements of both the acquiring and target companies to assess the financial impact and potential benefits of the transaction. It may include statements like the income statement, balance sheet, and cash flow statement. It is conducted to assess the overall financial health and performance of the company.

In investment banking, financial modelling is a crucial tool used in the financial statement analysis of a merger and acquisition (M&A). Investment bankers develop a merger model, which is a comprehensive financial model that projects the combined financial statements of the acquiring and target companies post-merger.

Cash Flow Analysis

Examining a company's cash inflows and outflows to assess its ability to generate and manage cash effectively. In investment banking jobs , one of the primary roles is to assess the transaction structure, including the consideration paid and the timing of cash flows.

Ratio Analysis

Utilising various financial ratios to interpret and analyse a company's financial performance, efficiency, and risk levels. Investment banking training equips professionals with a deep understanding of various financial ratios and their significance. They learn how to calculate and interpret ratios related to profitability, liquidity, solvency, efficiency, and valuation.

Comparable Company Analysis

Comparable Company Analysis (CCA) plays a crucial role in mergers and acquisitions (M&As) due to its importance in determining the valuation of the target company. In investment banking training , you will learn how to conduct a CCA and identify a group of comparable companies in the same industry as the target company.

By comparing the target company's financial metrics to its peers, you can identify the company's strengths, weaknesses, and positioning within the industry and provide appropriate guidance.

Discounted Cash Flow (DCF) Analysis

Discounted Cash Flow (DCF) analysis is a crucial valuation technique used in M&As. It helps determine the intrinsic value of a company. It helps project the potential cash flows of a company in the future. DCF analysis involves factors like revenue growth, operation costs, working capital requirements and the like.

Investment banking training provides the skills in building complex financial models that are required for DCF analysis. They develop comprehensive models that incorporate projected cash flows, discount rates, and terminal values to estimate the present value of a company.

Merger Consequences Analysis

Merger Consequences Analysis helps assess the potential outcomes and impact on financial performance, operations, and value of the entities partaking in the M&A. Investment bankers conduct an extensive evaluation to identify and quantify potential synergies that may result from the merger or acquisition, encompassing cost savings, revenue growth opportunities, operational efficiencies, and strategic advantages.

This analysis aids in estimating the financial implications of these synergies on the combined entity.

Legal and Regulatory Considerations

If you are pursuing an investment banking career , knowledge of the various legalities involved in M&As will help you nail any investment banking interview . The regulatory legalities involved in the process of M&As that partaking entities and investment banking services need to consider:-

Antitrust Laws and Regulations

Antitrust laws and regulations aim to foster fair competition and prevent anti-competitive practices. In the context of M&A, it is vital to assess whether the combination of the acquiring and target companies could potentially harm competition significantly.

Complying with antitrust laws may involve seeking clearance from regulatory bodies or implementing remedies to address any potential anti-competitive concerns.

Securities Laws and Regulations

Securities laws and regulations are of utmost importance in M&A transactions, considering the issuance of securities or transfer of ownership interests. Compliance with these laws governs the disclosure of material information, fair treatment of shareholders, and the filing of requisite documents with regulatory entities.

Regulatory Approvals and Filings

M&A transactions often necessitate obtaining approvals from various regulatory bodies, including government agencies, industry regulators, or competition authorities. These approvals ensure adherence to specific industry regulations and are typically indispensable for proceeding with the transaction.

Additionally, filings and disclosures like Form S-4 or 8-K, may be mandatory for furnishing relevant information about the transaction to legal authorities.

Confidentiality and Non-Disclosure Agreements

Confidentiality is crucial throughout M&A transactions. To safeguard sensitive information and trade secrets, parties involved usually enter into non-disclosure agreements (NDAs). These NDAs outline the terms and conditions governing the sharing and handling of confidential information throughout the entire transaction process.

M&A Documentation

The following M&A documents are instrumental in organising and formalising the holistic M&A process. They give clarity, safeguard the interests of all parties included, and guarantee compliance with pertinent legal and regulatory prerequisites all through the transferring process.

Letter of Intent (LOI)

The Letter of Intent (LOI) is the first and most urgent document that frames the agreements proposed in an M&A. It fills in as the commencement for exchanges and conversations among the gatherings participating in the business procedure.

Merger Agreement

The Merger Agreement is a legally approved contract that covers every detail of the merger. It may include crucial information like the price of purchase, terms of payment, warranties, post-closure commitments and representations. This arrangement formalises the responsibilities between the partaking parties.

Share Purchase Agreement

The Share Purchase Agreement is a legally binding contract that oversees the assets of the target organisation being acquired. It frames the terms, conditions, and legitimate liabilities connected with the exchange of ownership interests.

Asset Purchase Agreement

An Asset Purchase Agreement is utilised when particular assets of the target organisation are being gained. It is a legal contract that sets out the regulatory commitments attached to the procurement and division of those assets.

Confidentiality Agreements

Confidentiality Agreements, also known as Non-Disclosure Agreements (NDAs), play a major role in protecting sensitive data collected during the M&A cycle. They lay out rules and commitments to guarantee the safe handling and non-exposure of restrictive proprietary information and secrets.

Due Diligence Checklist

The Due Diligence Checklist is a broad list that helps direct the assessment process by framing the important documents, data, and areas to be evaluated. It works with an exhaustive and deliberate evaluation of the objective organisation's monetary, legal, functional, and business viewpoints.

M&A Case Studies

M&A case studies serve as a hub of knowledge, enabling companies to make informed decisions and avoid common pitfalls. By delving into these real-world examples, organisations can shape their M&A strategies, anticipate challenges, and increase the likelihood of successful outcomes. Some of these case studies may include:-

Successful M&A Transactions

Real-life examples and case studies of M&A transactions that have achieved remarkable success provide meaningful insights into the factors that contributed to their positive outcomes. By analysing these successful deals, companies can uncover valuable lessons and understand the strategic alignment, effective integration processes, synergies realised, and the resulting post-merger performance.

These case studies serve as an inspiration and offer practical knowledge for companies embarking on their own M&A journeys.

Failed M&A Transactions

It's equally important to learn from M&A transactions that did not meet expectations or faced challenges. These case studies shed light on the reasons behind their failure. We can examine the cultural clashes, integration issues, financial setbacks, or insufficient due diligence that led to unfavorable outcomes.

By evaluating failed M&A deals, companies can gain valuable insights so they can further avoid the pitfalls and consider the critical factors to build a successful M&A strategy.

Lessons Learned from M&A Deals

By analysing a wide range of M&A transactions, including both successful and unsuccessful ones, we can distill valuable lessons. These case studies help us identify recurring themes, best practices, and key takeaways.

They provide an in-depth and comprehensive understanding of the various pitfalls and potential opportunities involved in an M&A that can enhance their decision-making processes to develop effective strategies.

Taking up reliable investment banking courses can be instrumental in taking your career to unimaginable heights in this field.

M&A Strategies and Best Practices

By implementing the following M&A strategies, companies can enhance the likelihood of a successful merger or acquisition:

Strategic Fit and Synergies

One of the key aspects of M&A is ensuring strategic fit between the acquiring and target companies. This involves evaluating alignment in terms of business goals, market positioning, product portfolios, and customer base.

Integration Planning and Execution

A well-balanced integration plan is crucial for a successful M&A. It encompasses creating a roadmap for integrating the acquired company's operations, systems, processes, and people.

Effective execution of the integration plan requires careful coordination, clear communication, and strong project management to ensure a seamless transition and minimise disruption.

Cultural Integration

Merging organisations often have different cultures, values, and ways of doing business. Cultural integration is essential to aligning employees, fostering collaboration, and maintaining morale. Proactively managing cultural differences, promoting open communication, and creating a shared vision can help mitigate integration challenges and create a cohesive post-merger organisation.

Managing Stakeholders

M&A transactions involve multiple stakeholders, including employees, customers, suppliers, investors, and regulatory bodies. Managing their expectations, addressing concerns, and communicating the strategic rationale and benefits of the deal are all crucial.